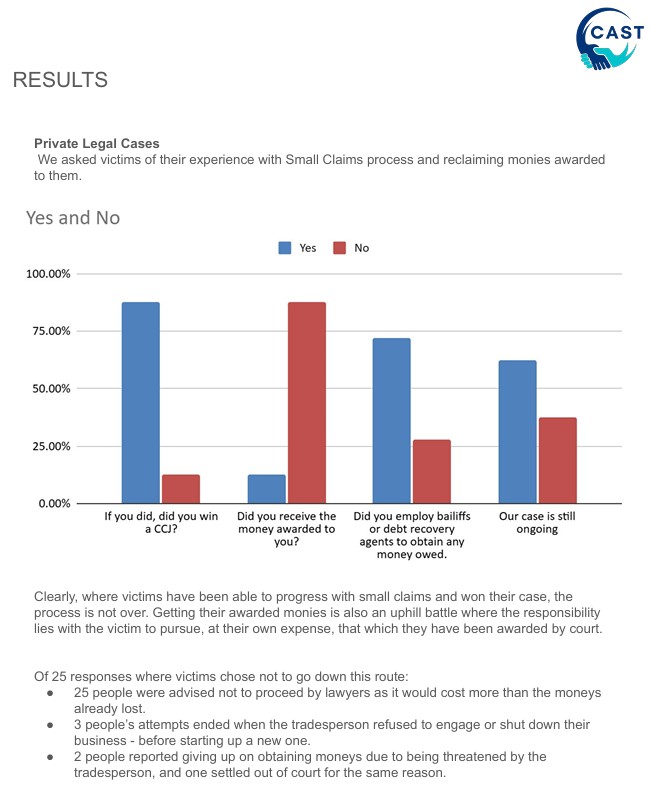

Survey results

Along with reading the Resolution pages, CAST recommends you also take a look at these survey results before making a decision on how to proceed. The full report can be read below.

January 2025 – March 2025

This report can be shared.

Along with reading the Resolution pages, CAST recommends you also take a look at these survey results before making a decision on how to proceed. The full report can be read below.

January 2025 – March 2025

This report can be shared.

If you feel things have gone wrong and you need help, or want your situation brough to light.

Contact

Their job: “…empower people by equipping them with the knowledge and confidence to navigate challenges they face”.

How they are set up: Citizen’s Advice across the UK are set up as different charities working under an umbrella national organisation. They have different contact numbers for each country in the UK.

They report back their data to a central location. The data is collated and used to identify areas of greatest need enabling Citizen’s Advice to provide help where it is needed.

What they can do: Provide you with template letters, let you know your rights and help you plan your approach. They are also the gateway to Trading Standards.

They can also support you if your trader has caused you to incur debt, by conducting a financial assessment and exploring possible solutions to help you recover.

What they cannot do: Take on your case for you, give legal advice or offer cancelling, while they can help you navigate debt issues they do not offer financial advice..

Where you may struggle: Getting through on the phone. Waiting times can be long. You can contact them online through the ‘chat’ function and fill in an online form between Friday 5pm and Monday 9am.

How to get through: Use the form to see if that helps, but keep persevering. Put the phone on speaker and get on with something else while you wait.

If everyone perseveres to get through, their central office data will flag rogue traders are an increasing problem, and Trading Standards will get more complaints about your rogue, which may trigger action.

Resources: Consumer Helpline Webpage; Debt Advice webpage

Their job: “…responsible for ensuring that businesses comply with trading standards legislation”. This covers ALL trading standards, not just skilled trades. if they feel it is in the public’s interest they can conduct criminal investigations and have a thorough, strict process to build a case for passing on to lawyers to take forward.

How they are set up: Primarily managed by local authorities in England, Scotland and Wales; Northern Ireland manages them centrally. To report a case to TS you need to contact Citizen’s Advice.

There is a National Trading Standards (NTS) that provides support and guidance to local authorities, particularly for issues that require regional or national focus. There is also a Chartered Trading Standards Institute (CTSI) involved in training, standards settings and advice.

What they can do: Investigate unfair or illegal business practises potentially leading to court action.

What they can’t do: Take up every case. Take up any case where there is no hard evidence. You will need to gather your evidence (scope, contract, texts/emails, photos etc) in order to be heard.

Where you may struggle: Getting them to take up your case. We hear there are inconsistencies across local authorities where some TS need between 1-2 people to report a rogue trader while others say 5-6 people are needed.

We hear TS have been badly impacted by budget cuts and lack of hiring over many years leading to a high burn out/resignation rate. This will impact their ability to take on cases.

We know that it is hard to start communications with TS and if your case is taken up the communication is poor to terrible.

Stay polite and friendly. We know how frustrating dealing with TS can be. Remain calm, remain polite, remain persistent.

Resources: Reporting to Trading Standards

Their job: “receiving and analyzing reports of fraud and cybercrime, and then forwarding them to the National Fraud Intelligence Bureau (NFIB) for further action” across England, Wales & Northern Ireland.

How they are set up: The UK’s national reporting centre, managed by the City of London Police and the National Fraud Intelligence Bureau (NFIB)

What they can do: Data synthesis and analysis to identify patterns and trends which are reported to the NFIB; they then use the data to identify potential leads for police investigations, block fraud enablers and provide police intelligence.

They can provide advice and guidance to the public including specific advice to people who have been victims of fraud. They can also connect victims to Victim Support for emotional and practical help.

What they can’t do: They do not have investigation powers, provide progress updates or help with fund recovery.

Where you may struggle: Getting them to take up the case. CAST victims are typically advised to report to Action Fraud to provide their data not necessarily to obtain help or support.

Resources: Their website

CAST recommend being careful with Facebook when things have gone wrong due as it could jeopardise your case if it progresses to court.

What YOU can do: Check Local social media site and rogue builder Facebook groups for your trader’s name, please do avoid naming and shaming your trader at this point. This might jeopardise your case. You can however ask if anyone has used your trader and see what feedback you get.

Find other people who the trader has done work for. Talk to their workmen, you might gain valuable information about who else they are working for.

The more people that report a rogue trader the more action trading standards will take. If they pursue a claim against your trader and win, you may be able to get your money back through your bank as your trader will have a criminal conviction.

Keep any exchanges or posts professional, factual and non-emotive.

What you shouldn’t do: Let your emotions take over and/or get involved in heated exchanges, give too much detail away (always think: could my sharing this jeopardise my case), respond to trolls.

Where you may struggle: You may be contacted by your trader who is likely to be unhappy about receiving negativity online. It may impact his business – and impact his ability to be a rogue. Review this page before making a decision on how to proceed.

Theses are the necessary steps to meet legal requirements, remove the trader from your site and start to move on.

Take a Breath – Don’t Panic

Don’t agree to pay anything straight away. Take some time to understand what’s going on and who is owed what.

A trustworthy trader won’t mind giving you a few days and answering your questions.

You have the right to take your time – don’t let anyone pressure you into a rushed decision.

Menu

Step 1: Check your Facts

Take time to check any contract or quote you have received for what is included and not included.

This is a good time to review the scope (all the work that was agreed) and the timescale it was agreed to be completed in.

Remember:

If you are going to terminate your contract with your trader, you need to do so legally, so follow the steps below to ensure you are complying the law. If you need to take your trader to court, this will work in your favour.

Resources:

Consumer Contracts Regulations (2013): https://www.which.co.uk/consumer-rights/regulation/consumer-contracts-regulations-ajWHC8m21cAk

The Consumer Rights Act (2015)https://www.which.co.uk/consumer-rights/regulation/consumer-rights-act-aKJYx8n5KiSl

Top tips:

Step 2: Document the Site

Take photos of how your home has been left, take photos of everything the contractor has done and a video if you can.

Top tips:

Step 3: Make it Formal

Remember:

If you can demonstrate that the trader has failed on one or more of these elements you may be able to remove them from site with breach of contract. Check your circumstances with Citizen’s Advice to ensure you get the wording right and can close the contract legally.

Resources:

https://www.citizensadvice.org.uk/consumer/template-letters/letters

Top tips:

Use Citizen’s Advice letter templates to make life easy for you. If you prefer not to then you will need to:

Step 4: Find a New Trader

If they do not respond or refuse to return after the 14/21 days have elapsed then you have the right to get someone else to complete the job/put right the poor workmanship.

You will need to obtain a couple (preferably 3) of written quotes from new traders.

If this costs you more than the quote from the original trader then you can try to reclaim the money from the original trader.

Remember:

You will need to obtain written quotations, if you want to try and reclaim money from the original contractor, these will need to detail the price and work to be undertaken.

Top Tips:

Step 5: Expert Evaluations

Consider the need for an expert witness report or a defects list.

These are reports that are completed by RICS Chartered Surveyors and detail the work that has been undertaken, the quality of the work undertaken and can look at the costs of the work and assess if there has been an under or overpayment/underpayment for the work. They can also look at the contract between yourselves and the contractor.

They are useful where you have had a large project completed with lots of complexity. For example, a single storey extension.

Resources:

https://www.rics.org/surveyor-careers/surveying/what-is-a-chartered-surveyor

Top tips

Summary

If your trader refuses to return to site to complete the work, you will need to get someone else to complete the work and then decide how you wish to try and recoup your additional costs, if the new trader has cost more. You have 6 years to do this, so don’t rush. Gather all your facts together.

Before you do any work, do consider the need for a RICS Chartered Surveyor, this will give you an expert witness report that is independent, if you do need to go to court. It can also give you an independent assessment of what has been done/not done.

Write to the trader (a letter is preferable, if you do not have their address, then send a screenshot of the letter to them or send it via WhatsApp or email) and tell them you have had someone else complete the work.

Be sure that the contract (even if it was a verbal contract) is closed and they have no valid reason to return to your site.

Give details of the additional cost you have incurred; you can include the quotation and copy of the invoice you have paid.

Ask the trader to refund you the difference between their original quote and the new quote that you have paid.

Tell the trader that if you cannot recoup the additional costs directly from them, then you will be left with no option than to go through the courts to refund your money.

Give them 14 or 21 days to respond to your letter.

If they are still refusing to settle with you, then you have the option of completing paperwork to take them to court.

If the value of the work is less than £10,000 you can use money claims online or the small claims court system. If the value of the work is over £10,000 then you will need to use the county court system.

Useful Link:

https://www.citizensadvice.org.uk/consumer/template-letters/letters

Top tips:

Critical facts:

If you and your lawyer agree there is a strong case with a good chance of recovery, this is the process:

Court Routes Available

There are several routes available within the civil court system and it will depend on the amount of money that you are owed.

Before you take your trader to court, you need to ensure that you have followed all the steps in ‘If it Has Gone Wrong’, this ensures that you are complying with your legal responsibilities.

Remember:

Please check the section on ‘deciding to pursue a claim’ before completing any court paperwork

Deciding which court you need.

The small claims court is designed for the lay person to use without the need for legal assistance.

If you need to pursue your trader through the fast track or multi track system it is likely that you will a solicitor. While there is nothing stopping you being a litigant in person (representing yourself) you will need to demonstrate a good understanding of the legislation that your trader has broken through argument against their lawyer.

You can choose to use the small claims court to recover part of the money owed to you from your trader, even if the total value is over £10k, as long as what you are claiming is not more than £10k.

You cannot put through multiple claims through the small court to equal the total owed.

Costs for small claims court

| Claim amount | Fees |

|---|---|

| Up to £300 | £35 |

| £300.01 to £500 | £50 |

| £500.01 to £1,000 | £70 |

| £1,000.01 to £1,500 | £80 |

| £1,500.01 to £3,000 | £115 |

| £3,000.01 to £5,000 | £205 |

| £5,000.01 to £10,000 | £455 |

| Over £10,000 | 5% of the total claim value |

You can also claim interest on the money that you are owed:

Claim the interest

Work out the interest

Source: https://www.gov.uk/make-court-claim-for-money/work-out-interest

Making a claim

Follow the link below:

Try the new online service – Your money claims account

You will be asked to answer a series of questions to determine if you can make an online submission. This is based on the amount you are claiming, who you are claiming against and the amount of people you are claiming for.

You cannot use this service:

Or you can complete a paper form and submit to the court.

Follow the link below to the form:

There are also some notes to help you complete the form:

https://assets.publishing.service.gov.uk/media/664caaaaf34f9b5a56adcba2/N1A_0524.pdf

Useful link:

This is a helpful video on completing the small claims form.

Remember:

What to do after you have completed the form

You need to produce a copy of the claim form per defendant and one for the court, you need to then either send your form electronically or by post to the court.

Step 3: After submitting the claim form

The defendant then has 14 days to respond from when the court issue the paperwork to respond.

They can respond with an ‘acknowledgment of service’ this means that they acknowledge that they are received the paperwork but that they need more time to respond.

If they send you an acknowledgement of service, they have 28 days to send you a reply. The 28 days start from when they receive the details of your claim.

If you used Civil Money Claims, the defendant has 19 days from the day the claim is made. If they need longer, they must tell the court. The most they can have is 33 days

Both you and the trader will be offered a mediation session with a court appointed mediator. Do take this opportunity, as it will not be looked upon favourably by the court if you refuse to attend. These appointments are usually by phone/video conferencing.

Sometimes a mediation session can help to resolve your claim, if it does not resolve the claim then a court date will be issued.

Step 4: Going to court

Gather all evidence, emails, texts etc- anything to do with your case and categorise it. You want to make it easy for a court to look at your evidence and see the story of what has happened.

You and the defendant will be in a meeting room with the judge, who will look through all the evidence and ask questions of both you and the trader.

Do:

Remember:

The court won’t know your story, make sure that everything is easy to find in order of what has happened and when and ensure that it tells the story from beginning to end.

Step 5: The Judgement

At the end of the case, the judge will make a judgement. If this is in your favour then the trader will have a CCJ awarded against them. This means that you can now collect the money you are owed.

Step 6: Getting Payment

You now have a judgement against your trader, great, but how do you go about getting payment. Hopefully your trader will be ready to admit that they owe you money and will pay without further issues. However, that is rare. There are now several options open to you.

Debt collectors

You can appoint high court enforcement officers/debt collectors to collect the debt on your behalf, they will charge fees for the collection and this can be added to the debt that the trader owes you. They usually work on a commission basis. There are numerous debt collectors to choose from, but we would recommend using a debt collector that is FCA (Financial Conduct Authority) registered.

Bankruptcy

If your trader refuses to pay or debt collectors are not successful in obtaining your money, then you can apply to make your trader bankrupt. This would mean that you would need to present a bankruptcy petition to the court.

The fee for doing this is £1,500 plus £343 in court costs

Useful link:

https://www.gov.uk/apply-to-bankrupt-someone/apply

Charging order

This is a court order that secures the debt against your traders property, for example their home. This means that if the trader sells or remortgages their property, then the money from the sale of the property will be used to pay off the debt owed to you.

If you have won a CCJ against your trader, then it may be worth considering registering the interim charging order at HM Land Registry after you have a judgment. This will make sure the order is effective immediately. This could be useful if you don’t think you trader will pay or will move titles of ownership before you can collect payment.

There is a fee to be paid to raise a charging order on a property. This is an initial fee of £110. If the charging order is granted this can be recovered from your trader.

Useful link:

If you decide to pursue a claim against a trader, you must follow the steps in ‘If it Has Gone Wrong’ to comply with the law. If you don’t, you could jeopardise any court case you later want to raise.

you need to understand if a claim is wroth pursuing. Does the tradesperson have assets that can be claimed against?

Company Type

Are you dealing with a sole trader or a limited company (Ltd)?

Sole traders have unlimited liability, so therefore if they have assets, such as property in their name or equipment in their name and owned by them, then there is potentially money to be claimed against, if they own their own property/assets.

Limited companies have limited liability, this means that the liability for any issues stops with the company and cannot be transferred to an individual, therefore a trader can dissolve their company and therefore have no assets to be claimed against.

If the company has a default address, which is currently

The main reasons for this address is that either a person or business has complained that the company is not authorised to use the address they provided. This could indicate that you have an issue with your trader.

Top tips:

If you are dealing with a limited company and you think they are about to go into liquidation and they owe you money, you can apply to Companies House to the company being struck off the register of companies.

You can also make contact with the liquidator and ask to be listed as a creditor to the company.

Resources

https://www.gov.uk/get-information-about-a-company

https://find-and-update.company-information.service.gov.uk/strike-off-objections

Check for CCJ’s against the person/trader

One way to check a company’s or person’s history is to run a County Court Judgement (CCJ) check.

Resources

Check the land registry

If your trader is a sole trader, you can check the land registry to see if they own property. This costs £7.

You will need to know your traders name and home address to do this.

Resources

https://www.gov.uk/search-property-information-land-registry

Identify the right court route

All are part of the county court system, you will be allocated a track based on the value you are claiming.

For further details on the court system and its associated costs, please see the section on ‘taking your trader to court’.

Top Tips

Make sure your trader has assets in their own name. You want to recover money, not collect CCJs or spend more money on debt recovery people.

Ensure your solicitor provides estimated legal costs for your case and make sure you see their T&C’s on billing.

You must follow the steps in ‘if it has gone wrong’ to comply with your own legal obligations.

Mediation

With small claims you are required to go through mediation before going to court.

If you are seeking more than £10,000 you may be offered mediation (the court will organise this) or you can chose private mediation.

https://www.gov.uk/respond-to-court-claim-for-money/mediation

Consider if you can claim your money back from your bank

If payment has been made via bank transfer which is now viewed to be the norm, it is important to know if your bank has queried uncharacteristic transactions.

If no contact has been made you, the account holder, could pursue a claim the bank has not followed the ‘banking protocol’ under the CRM (Consumer Reimbursement Model) Code.

The maximum that can be claimed from a bank is limited to £85k. If per chance payment was made via a credit card, the value of the transaction being no more than £30k, the credit card provider can be held jointly liable as per The Consumer Credit Act 1974 S.75

Consider registering your claim with your bank, if you feel that the bank has not done enough to protect you the consumer.

Resources

Once you have checked all these steps, please go to the section on ‘taking your trader to court’

Issues that can occur when in dispute with a trader

A dispute with a trader can be upsetting and very stressful. Things can get ‘ugly’ while remaining civil, adding more stress to an already challenging situation.

CAST will never suggest nor recommend actions that break the law. Ensure you remain factual, non-emotive and communicative. Remove yourself from any situation where you feel you may lose control or say/do something you will regret.

Here are some common problems you might face with a rogue trader and the tricks they may use to get more money or avoid being held accountable.

Contents:

Debt collectors/ Debt collecting solicitors can be appointed by anyone to pursue a debt that someone feels that they are owed, that doesn’t mean they are always entitled to the money.

Check this section to judge if your trader has completed what was quoted and that the work is to a good standard.

You are under no legal obligation to pay a debt collector, unless the person who you owe money to has obtained a CCJ (County Court Judgment) against you. This requires the trader to take you to court for non payment of an invoice first.

See Top Tips on what to do if Debt Collectors arrive at your door.

If you have received a letter from a debt collector.

You have 30 days to respond to a letter from a debt collector. Do not ignore it. Take your time and use this time to gain legal advice and check the details, there is no need to panic, they can only ask for the money, they have no power to compel you to pay.

Do take the time to check if your debt collector is FCA registered, be wary of those that are not.

If you have not received a satisfactory service from your trader and you receive a letter, it is OK to ask for further clarification and to say that the sum requested is in dispute.

Remember

If the work has not been completed to a decent standard and/or your trader has not completed the work, you do not have to pay. You can say that the amount is ‘in dispute’ and ask for further clarification.

Any reputable trader will be happy to come back and fix any errors/omissions before receiving payment.

Make sure you have followed the section on if it has gone wrong to ensure that you are complying with the law.

Contact your house insurance. Many insurers provide a free legal advice line and depending on your insurance may be able to provide you with a solicitor.

Top Tips: Dealing with Debt Collectors

Bailiffs have legal power, are registered and are authorised to enforce Court Orders.

Debt Collectors do not have this power, typically work on behalf of creditors or debt collection agencies. Their focus should be on negotiating payment arrangements.

If you do not have a CCJ against you and a debt collector has arrived at your door:

Resources

https://www.fca.org.uk/firms/financial-services-register

Citizen’s Advice: Stopping Bailiffs At your Door

If you receive a letter from a solicitor from your trader. Don’t panic and take the time to check the correspondence carefully.

Check the content of the letter to check if it looks like a solicitor’s letter. Look for the language used, grammar, spelling and punctuation. Does it look like a real letter?

Solicitors will send you a postal letter in a dispute situation, they do not attach a letter to an email.

It is a legal requirement for solicitors to be registered with the Solicitors Regulation Authority, who will issue them with a Solicitors Regulation Authority (SRA) number. You can confirm the letter solicitor’s details and their SRA number with the SRA under ‘Solicitors Register’ . Any genuine solicitor will include this on their letters to you.

You have 30 days to respond to a letter from a debt collector solicitor, please do not ignore it. Take your time and use this time to gain legal advice and check the details, there is no need to panic, they can only ask for the money, they have no power to compel you to pay.

Remember

If your work has not been completed to a decent standard and/or your trader has not completed the work, you do not have to pay. You can say that the amount is ‘in dispute’ and ask for further clarification.

Any reputable trader will be happy to come back and fix any errors/omissions before receiving payment.

Make sure you have followed the section on if it has gone wrong to ensure that you are complying with the law.

Contact your house insurance many insurers provide a free legal advice line and depending on your insurance may be able to provide you with a solicitor.

Resources

The Defamation Act (2013) was introduced in order to reform the law surrounding defamation and to ensure that a fair balance between the protection of reputations and freedom of expression was being attained.

The aim of the Act is to redress the imbalance that existed between the protection of reputations against defamation and freedom of speech before its introduction.

CAST recommends caution about naming and shaming your trader if you are planning on going to court as it may prejudice your case. However, section 2 and 3 of the Act make provision for truth and honest opinion.

Therefore, if you are providing a review of your trader ensure that your review is factual, non-emotive and can be substantiated with evidence.

Resources

A really interesting overview of Libel & Slander and the distinction in Defamation,

If your trader provides you with a ‘quote’ it is a fixed price for the job and they should not be charging you more money, unless you have asked for them to do extra work or they have uncovered a problem while undertaking the work.

An ‘estimate’ is a price for a job that may rise or fall depending on what is found when the job is progressing.

If they have uncovered a problem and extra work is required, they should have provided you with a written quote before undertaking that work if the work is valued over £42, whether it is a quote or estimate.

There should have been a written agreement from you that they can undertake the extra work and they should have offered you a 14 day cooling off period.

Any reputable trader will give you time to consider their quote/estimate and will not pressurize you into agreeing quickly. You have the right to consider their new quotation/estimate.

Resources

Consumer Contracts Regulations (2013)

https://www.which.co.uk/consumer-rights/regulation/consumer-contracts-regulations-ajWHC8m21cAk

The Consumer Rights Act (2015)

https://www.which.co.uk/consumer-rights/regulation/consumer-rights-act-aKJYx8n5KiSl

If they are charging you VAT check they are legally allowed to do so. If they are not VAT registered you do not have to pay VAT.

If they say they are in the process of going through VAT registration, which is a valid reason to not have a VAT number, you can withhold the VAT until they can produce (and you have checked) a valid VAT number.

Police will state that an issue between you and your tradesperson is a civil matter and will not take up the case.

Receiving threats or hate speech from a tradesperson is not a civil matter. You can report these to the police and insist on a case number. Keep a record of this number as every matter that arises can be added to that number, creating a solid record.

If you are feeling threatened by your trader, ring 111 immediately and report them. If you are in immediate danger call 999.

You can take additional steps to protect yourselves by

Contact trading standards to report your trader if you are feeling intimidated or you feel they are not treating you fairly. You can do this through Citizens Advice. They may already be aware of your trader.

Resources

https://www.citizensadvice.org.uk/consumer/get-more-help/report-to-trading-standards

Rogue Traders will sometimes threaten court action to try and encourage you to pay. If you find yourself on the receiving end of one of these messages, then please follow the section on ‘if its gone wrong’

Take your time to assess the situation before taking any immediate action. A reputable trader will wait and will not pressurize you into action.

Check if you have legal cover through your house insurance, many home insurers will provide you with a solicitor or a legal advice line.

Remember:

Communication with your trader is key. Keep all communication written from this point in, preferably by email.

Keep all communication with your trader factual.

Do not be pressurised into making a decision. Courts will not penalise you for this.

Research and really think about what you want. The more you are well prepared the better. Don’t leave the tradesperson to guess.

These are jobs requiring a single tradesperson, like routine maintenance. This can also be a small specific piece of work like replastering a whole room or knocking through a wall to merge two rooms.

Identify and write down what you want in simple, straight forward terms. It is worth taking some time to research what other people do as you can get tips you may not think of.

Write down if you have critical dates or timescales. Don’t take a guess at how long the job will take or how much it will cost. You cannot be the buyer and the seller. That information is for the tradesperson to provide and from that you can measure what the average is.

Don’t mention your budget.

These are projects where you are using significant savings and / or taking out a mortgage to pay for the works.

If you are working on a larger project with a Principal Designer (ie: an architect) on a larger project write down notes on how you would like the changes to your home to improve how you use the house.

You may wish to develop a mood board to help you visualise your goals and for a Principal Designer to understand the design you are hoping for.

Indicate your rough budget; the architect should be able to advise if your hopes are affordable within your budget or not.

Top Tips

The day your work starts is a few weeks away, now the work starts.

Kick Off Preparation

Supervision & Inspections

Sign Offs and Close Out

Make sure they are aware of the works and notify them of the start date and the tradesperson’s details if they have not already got this.

About two weeks before kick off, meet your tradesperson/people to outline what they expect on day 1.

Align on how you will be communicating when issues arise (they WILL arise) and review the early milestones and timescales.

NOTE: if the project start has been delayed the milestone date will need updating and re-issuing as a new version.

Take minutes of the meeting in your diary, it is polite to share this with the builder.

Top Tips

Update that Diary!

This will be your record of progress, agreements, decisions, instructions and performance.

If it all goes wrong this diary is a big chunk of your evidence.

Photos:

Every week, go to site and take numerous photos of each room/area, including items delivered and any rubbish to be disposed of.

Ensure the photos are clear and represent a true likeness.

Doing this creates a progress record and highlights any issues and successes.

Download and file these images in your diary/filing asap. Do it each week for ease now, and easier reference later on if needed.

Walk the total site with the tradesperson and make a note of any areas of concerns, discuss them immediately and update your diary of any decision or if conversations need to continue on that topic. Always follow up with the tradesperson in writing.

Keep it up! There will come a time when it feels pointless, it isn’t, it’s really valuable.

Dos & Don’ts

Top Tips

Progress photos:

There will come a time when you feel like it will never be over and need to look back to see how far you have come.

Keep it up! If it all hits the fan you’ll need all photos and conversation records as evidence.

This is where you create a list of fixing final, minor issues (snags) before closing the project an getting your home back.

Typically snagging takes place in the final Inspection phase and must be completed before certification and final payment. This is where the retention fee agreed in your contract comes in to play.

The goal of snagging is to ensure the building is safe, functional, and aesthetic.

Snags can range from minor cosmetic issues to more serious structural problems. Some examples of snags include:

How to do Snagging

Let the tradesperson know you will be getting the snagging list to them by a specific date.

Walk the project with your trusty notebook and note down everything that catches your eye. In addition to the list on the left, consider:

Produce a list for the tradesperson to review and together agree dates to complete the work.

Top Tip

Snagging is not the time to raise a big issue that should have been raised in a weekly inspection (ie: the kitchen plan shows a gas cooker but no gas outlet has been installed)

The tradespeople will want to move onto their next job so will want the snagging completed asap so they can get their final payment and move on.

Write the list once only. Be thorough the first time ‘round so a complete list can be provided and worked through.

Legally required

Make sure these are required by the relevant, qualified expert (ie: electrician, building control), that certificates are handed over before final payment.

No legal requirement (ie: plasterer)

Sign off can be down to a chosen third party (ie: a project manager or your architect) to do this. If you are running the project yourself you will need to sign off the non-legal areas.

You will also need to approve the snagging list is complete.

Process payment asap, without delay and without fail.

Congratulations – you did it!

Top Tips

Some tradespeople will not release the certificate without final payment.

This is typically because they have encountered Rogue Customers and built this into their processes.

Or they are Building Control, who also operate on a payment first process.

There are times you will have to trust.

Congratulations! You made it, you have closed out your project.

When you have chosen your Tradesperson and received their cost proposal you need to check if the price is actually a quote, and estimate so something else. There are different methods of pricing a job which will impact how the project is managed and also how much you actually pay.

This section will inform you about the different types of pricing you may encounter.

Top Tip

Ask what quality the tradesperson provides costs for. They may provide an entry level/basic finish cost whereas you are expecting a higher level finish. Example: You want porcelain tiles at £50 per square metre, and they typically cost for £25 per square metre. Discuss this early to avoid assumptions and confusion.

Pricing Methods

Pricing Assessment

Payments

Preferably a document a builder gives to a client, stating the cost of goods or services before the client decides to buy.

It includes the price and terms of the offer.

Quotes let the client know how much they will need to pay, so there are no surprises when they agree to the service or purchase.

Good for

Small works such as routine maintenance and a single, non complex task

Beware!

Verbal quotations need to be backed up in writing or text; if they do not send one through within 48 hours of providing a quote, send through a confirmation of your conversation and the quoted amount.

If you add any new items to the scope after costs have been agreed, none of this work has been quoted for, will incur extra costs and may cause missed timelines.

If your work uncovers an issue that had not been anticipated by the tradesperson (ie: dangerous cabling) you will need to discuss options and costs on site. This will cost you more though you need to understand impact to cost, time and if there is any knock on effect to other areas of the property (See Managing Scope Creep section )

A document given to a customer showing how much the tradesperson thinks they will be charging for the goods or services.

It is not a final price, so the actual cost can be higher or lower when you send the invoice.

Before accepting an estimate, it’s important to understand what you’ll be charged for things like labour, profit, and any added costs on materials.

Good for:

Small works such as a new flooring finish or medium works such as a wall removal or a room refurbishment where works may be uncover hidden issue(s) that need working on; as with Quotes you will need more information to make an informed decision and control costs.

Beware

Estimates are rough and may be exaggerated to avoid potentially difficult conversations if the cost needs to go up. Understand what you are being charged for.

If a contractor exaggerates as written above and you accept the estimate, they are allowed to charge the initial estimate amount even if it is far more than the works needed.

A Provisional Sum (PS)

An allowance (best guess) amount, usually estimated by a consultant. A provisional sum is an estimated amount set aside in project documents for work that hasn’t been fully defined or costed yet.

Typically included in a fixed price (lump sum) proposal and will cover items that cannot be costed effectively this early in the process.

When the work is done, the actual cost will replace the provisional sum in the contract, and the total price will be adjusted accordingly.

Provisional sums account for both the item’s cost and any work related to installing or completing it, ensuring flexibility for items that are yet to be clearly specified.

Tradespeople can include a provisional sum in their response or costing for work elements that lack sufficient detail for precise pricing (e.g., estimating the cost of a bespoke kitchen before final designs are confirmed)

Good for:

Projects with multiple/more than one skilled tradesperson and where you are investing savings or getting a mortgage to cover the costs.

You can ensure that your whole scope is included and which costs may change. It’s worth asking if a ballpark range can be provided which can help with your costings and expectations.

Beware

Where a lump sum (total price) contract provides a provisional sum the final amount payable will be adjusted to reflect the actual cost of the work.

As the unknowns become known, ensure you discuss solutions and cost / time impacts with your builder before they continue work or racking up costs.

Your contract needs to stipulate that the tradesperson must provide options for each solutions and time/cost impact for each, this will enable you to ask further questions and make an informed decision; and that the tradesperson is not to proceed until they have received formal instruction to do so.

When making a decision, make a note of the conversation details and your decision/instruction and follow up in writing each time.

A PC Sum is a budget set by the Quantity Surveyor or client for the supply-only cost of materials or goods. For example, if you know the area of tiles needed for a bathroom, you might allow £35/m² for tiling. PC Sums are used when the exact quality or specification of materials is unknown at the time of pricing.

Traditionally, they cover only the cost of the item itself, not related work such as installation. PC sums are used when the exact type or quality of materials isn’t decided yet.

Good for:

Large projects where the design is not finalised yet or where the customer has ordered elements of the project (ie: you bought the bathroom suite)

Beware

This is a high risk option for a domestic project.

A PC sum excludes the cost of labour installing or working with those materials.

Make sure you get labour cost estimates included in the cost proposal.

This route will require close cost management throughout the entire project as there is a risk of costs spiralling.

A PC Sum also comes with legislation that holds the customer responsible for the performance of a subcontractor instead of the responsibility being the main contractor. That means that the customer is held responsible for any delays caused by the sub contractor

The cost proposal needs to show:

If the cost proposal has the above and you have not already done so, now is the time to carry out the list of checks you can do online:

If they pass the online checks and you want to proceed to a shortlist, ask for:

When to reject a quote

Top Tips

If the quote comes in higher than expected across all tradespeople there are somethings you can do as part of negotiations:

Once you have refined your quote and selected your tradesperson you need to agree payments.

Recommended Stage Payments.

Note

There are so many possible variables for this page we are starting with the most common as a baseline.

As we hear feedback on different scenarios we can update this page accordingly.

We currently have a gap in this area and are working to close it.

CAST recommends getting a contract in place and getting a contract lawyer to conduct this piece of work, particularly if you are using savings/taking out a mortgage to cover the work.

You will also be able to raise your concerns and any elements you want included in the contract, ensuring that wording is in place to protect you as much as possible.

While off-the-shelf contracts are available the more you are spending on your project the greater the benefit of seeking a tailored contract that represents your interests.

A contract will not stop a rogue. It will enable you to manage a good tradesperson and, if it goes wrong, ensure you can get rid of the rogue due to clear breach of contract. If you chose to progress to small claims it will clearly demonstrate where the contract was breached and with Trading Standards what the tradesperson had legally agreed to do vs what they actually did.

Principle Designer

Under the new Building Control laws if you need Building Control to sign anything off, you will need a Principle Designer.

A Principle Contractor (builder) can be both principle Designer and Contractor ie: knocking two rooms into one.

If you need, or want a separate Principle Designer and/or have a project that requires construction drawings there are two routes:

What is the difference? Both can be creative and have great design ideas and each have their own code of conduct, governing body and associated requirements they need to meet in order to practise.

Ultimately, you need to chose someone you can build a rapport with. They will be interpreting your ideas and proposing some of their own.

Focus

Architects focus on the aesthetics and structure of buildings

Responsibilities

Architects design, plan, and supervise. They can manage the planning permission process for you.

Training

Architects are generally more design-led

Licensing

The term ‘architect’ is a legal definition.

Architects are governed by RIBA (Royal Institute of British Architects) and must be registered with the Architects Registration Board (ARB). If they are not registered, they are not legally an architect.

They must adhere to a professional code of conduct and can be reprimanded if they are found guilty of negligence.

Architects

Top Tips

Resources

Focus

Architectural technicians focus on the more practical aspects.

Responsibilities

Architectural technicians organize technical data, develop specifications, and create construction plans. They can manage the planning permission process for you.

Training

Architectural technologists have more experience and training in the science and technology of buildings.

Licensing

Technicians are governed by CIAT (Chartered Institute of Architectural Technologists), are not licensed professionals, but they can become certified in their field of expertise.

Critical Checks

Check your Architectural Technician is a member of CIAT and meets their requirements of excellence, ethics and accountability by checking their membership status..

Architectural Technicians can also qualify as a CIAT Registered Principal Designer

Get copies of their Personal Indemnity Insurance (PII) certificates to be sure you are protected

Top Tips

Resources

What do you want to do?

Be specific.

What is your aesthetic

What do you want them to do?

Top Tips

The cost of hiring someone to manage the process and people could be far less stressful than trying to do it yourself in addition to a full time job.

The costs could be a small percentage of the total project costs and a worthwhile investment.

Scope refers to a Scope of Work. it is a document that outlines a project’s objectives, deliverables, timeline and ,milestones.

It is a critical document that:

Top Tip

You can write your own scope and for a small job this is sensible and achievable. If this is new to you or you are investing a your savings or getting a mortgage for this project it is worth hiring the Principle Designer to create one for you.

Milestones to date are critical as they can be tied to stage payments, used to formally remove a rogue from the site and close the contract under breach of contract.

If you are going to write your own scope, use these headings. Be sure to include common Milestones.

1. Pre-Design/Feasibility Stage

2. Schematic Design

3. Design Development

4. Construction Documents

5. Construction Administration

6. Post-Construction

Each phase ensures the Principle Designer is involved from concept through completion, safeguarding the project’s integrity and client satisfaction.

What is scope creep?

Scope creep is when there is a deviation from your original written scope that has been costed against.

A deviation can occur because:

Who can agree scope creep?

How to manage scope creep

In all instances you the customer need to receive the options that are open to you, the cost and time impact.

You must have this to make an informed decision – and understand the impact of what you are agreeing to.

Always document the options, cost, time impact of the options you chose by confirming in writing to the Principle Designer/ Contractor AND updating your diary and your budget.

Top Tips

A milestone is a key point in a project that shows important progress. With target dates, they give everyone involved clear goals to track whether the project is on time and going as planned.

Milestones are often connected to finishing a specific part of the project, like completing the design or starting construction.

Common Construction Milestones Include:

1. Project Kick-Off: The official start of the project, where initial plans, roles, and expectations are laid out.

2. Design Completion: The point at which all design-related documents, drawings, and approvals are finalized.

3. Permitting: Obtaining the necessary legal permits from local authorities to begin construction.

4. Site Preparation: When the construction site is cleared, excavated, and made ready for building.

5. Foundation Completion: The completion of the foundational work, such as laying concrete footings or slabs.

6. Framing Completion: When the building’s basic structure or framework is finished.

7. Rough-In Inspections: These inspections occur when systems like plumbing, electrical, and HVAC are installed but before walls are closed up.

8. Substantial Completion: The stage when the construction is almost complete and the project is ready for occupancy, pending minor adjustments or final inspections.

9. Final Inspection: When the building is inspected for compliance with codes and standards.

10. Project Handover: The official transfer of the completed project to the client, including all documentation and warranties.

Milestones help project managers, architects, and stakeholders stay on track by providing clear, measurable goals throughout the project.

Top Tips

Milestones with target dates are critical